Every Canadian small business owner who drives for work — whether you visit clients in Kanata, deliver around the Ottawa core, or run a trade truck across Eastern Ontario — can claim a vehicle tax deduction in Canada. The catch is that the Canada Revenue Agency (CRA) is unusually strict about how you split personal versus business use, how you log your kilometres, and which receipts actually qualify. Get it wrong and the CRA will reassess your return, charge interest, and disallow the deduction entirely.

This guide breaks down the 2026 CRA rules in plain English: what you can claim, how to track it, the new dollar limits, lease versus purchase math, and the mistakes that trigger audits. Use it before you file your T1, T2125 or T2 — and bookmark it for next year.

Table of Contents

Key Takeaways

- The vehicle tax deduction in Canada is calculated as (business kilometres ÷ total kilometres) × eligible expenses — not as a flat dollar amount.

- For 2026, the CRA capital cost ceiling on a passenger vehicle is $38,000 before tax, and lease deductions are capped at $1,100 per month before tax.

- You must keep a kilometre log for every business trip; the CRA accepts a sample-year log only if you have a full base-year log on file.

- Driving from home to a regular office is personal use, not business — even if you own the company.

- Zero-emission passenger vehicles (Class 54) qualify for an enhanced first-year CCA up to a $61,000 ceiling.

What Counts as a Deductible Vehicle Expense

A vehicle tax deduction in Canada covers the cost of operating a motor vehicle for the purpose of earning business income. CRA splits the eligible costs into two buckets: operating expenses (the cash you spend running the vehicle each year) and capital cost allowance, or CCA (the depreciation of the vehicle itself).

Operating expenses that qualify include:

- Fuel and oil

- Maintenance and repairs (oil changes, brakes, tires)

- Licence and registration fees

- Insurance premiums

- Lease payments (subject to the monthly cap)

- Interest on a loan used to buy the vehicle (subject to a monthly cap of $350)

- Eligible parking when meeting clients or working off-site

- Toll charges (Highway 407, bridge tolls, ferry crossings)

- CAA or roadside assistance memberships used for the business vehicle

What you cannot deduct: traffic and parking fines, the cost of commuting between home and your regular place of work, and any personal-use portion of the above.

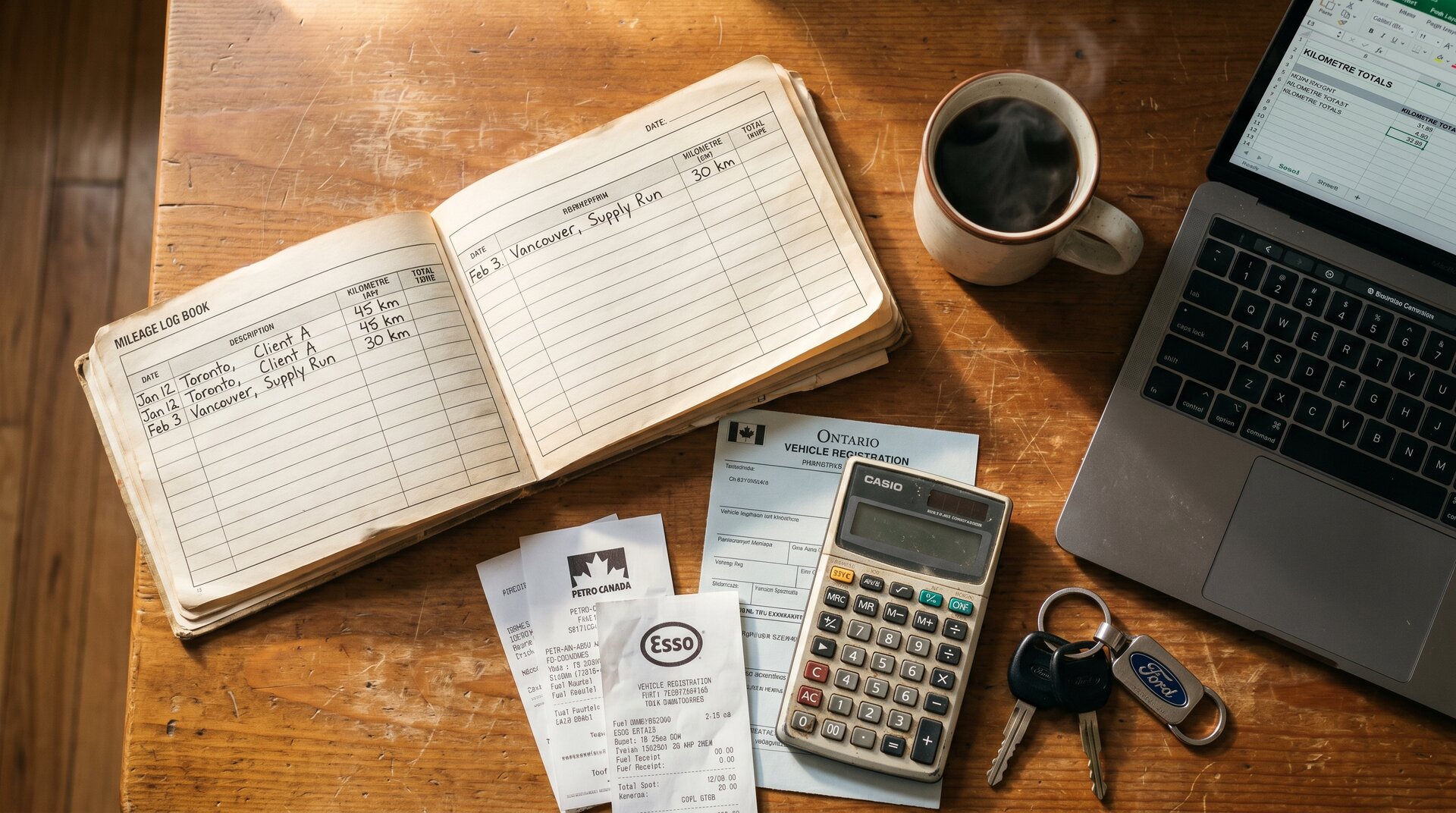

The CRA Log Book: Personal vs Business Use

The single most important habit for any vehicle tax deduction is the log book. CRA requires a record of every business trip showing the date, destination, purpose, and kilometres driven. Total kilometres come from your odometer reading on January 1 and December 31.

The CRA does allow a simplified three-month sample log in later years — but only if you maintained a full 12-month base-year log first and the business use of the vehicle stays within 10 percentage points of that base year. Without a base-year log, the sample method is not available and the CRA can disallow the entire deduction.

Critically, the trip from your home to a “regular place of employment” is personal use, even for an incorporated owner-operator. Travel between two work sites, to a client, or to a supplier counts as business. This matters because BBA Tax has seen Ottawa contractors lose deductions worth thousands simply by claiming their daily commute. If you split personal and business expenses on more than just your vehicle, our guide on separating personal and business expenses is a useful follow-up read.

Operating Expenses vs Capital Cost Allowance

Operating costs are deducted in the year you incur them; the vehicle itself is capitalized and depreciated over several years using CCA. Most passenger vehicles fall into Class 10 (30% declining-balance) or Class 10.1 for vehicles purchased above the CCA ceiling.

The half-year rule applies in the year of purchase — you can only claim 50% of the normal CCA in year one. The Accelerated Investment Incentive, which boosted first-year CCA on most assets, was fully phased out at the end of 2024, so 2026 acquisitions are back to standard rates.

Zero-emission passenger vehicles get separate treatment in Class 54 with a higher capital cost ceiling and an enhanced first-year deduction — covered below.

Not sure whether your vehicle should sit in Class 10 or 10.1, or how to back-calculate the CCA you missed last year? BBA Tax handles vehicle deductions for Ottawa-area sole proprietors and incorporated contractors every week. Book a free 15-minute call and we will tell you in plain numbers what you can claim.

2026 CRA Vehicle Limits and Rates

The Department of Finance Canada publishes the passenger-vehicle deduction limits each December. For purchases made in 2026, the figures small businesses need to know are:

| Item | 2026 Limit (before GST/HST/PST) |

|---|---|

| Capital cost ceiling — passenger vehicles (Class 10.1) | $38,000 |

| Capital cost ceiling — Class 54 zero-emission passenger vehicles | $61,000 |

| Monthly lease deduction limit | $1,100 |

| Monthly interest deduction limit (new loans) | $350 |

| Per-kilometre tax-free allowance to employees (first 5,000 km) | 72 cents |

| Per-kilometre tax-free allowance to employees (after 5,000 km) | 66 cents |

Source: the official limits and rates are published by the Department of Finance Canada and administered by the CRA. Always check the current-year notice before you file — Finance can adjust these limits year over year as it did in 2023, 2024 and 2025.

Lease vs Buy: Which Deduction Wins

There is no universal answer — it depends on the vehicle price, how many business kilometres you drive, and how long you keep the vehicle.

Lease: Monthly payments are deductible up to the $1,100 cap. The cap is applied through a CRA formula that also limits the deduction once the vehicle’s manufacturer list price exceeds the prescribed amount. The lease deduction usually wins for high-end vehicles driven heavily for business in the first 3–4 years.

Buy: You claim CCA based on the capital cost (limited to $38,000 plus tax for Class 10.1), plus interest on the loan up to $350 per month. The buy deduction usually wins when you keep the vehicle longer than 5–6 years, and especially when you finance with cash or a low-rate loan.

Run the math both ways before you sign. Many of our incorporated clients combine the vehicle decision with their broader corporate tax planning — see our corporate tax services page if you would like that done for your fiscal year-end.

EVs and Zero-Emission Vehicles (Class 54/55)

Buying a battery-electric or eligible plug-in hybrid? You may qualify for Class 54 (passenger) or Class 55 (taxi/leasing) treatment, which the federal government introduced to accelerate the EV transition.

Highlights:

- The capital cost ceiling for Class 54 passenger vehicles is $61,000 before tax — significantly higher than the $38,000 ceiling for traditional passenger vehicles.

- The enhanced first-year CCA rate that allowed up to 100% write-off was fully phased out at the end of 2027 for property available for use in earlier years; for 2026 acquisitions check the current CRA schedule before claiming.

- The federal iZEV purchase incentive program was paused in January 2025 and replaced with provincial programs — Ontario currently has no provincial EV rebate.

EV charging equipment installed at your business location is treated as a separate Class 43.1 or 43.2 asset, not bundled with the vehicle.

Common Mistakes That Trigger CRA Audits

- Claiming 100% business use. Unless your vehicle is a dedicated delivery van, a 100% claim is a near-instant audit flag. CRA expects a realistic split with documentation.

- Estimating kilometres instead of logging them. “Roughly 25,000 km” is not a log. Use a phone app (MileIQ, TripLog, QuickBooks Mileage) or a paper notebook in the glove box.

- Claiming the commute. Home-to-office is never deductible, even if your office is rented in your name.

- Forgetting the GST/HST input tax credit. The business-use portion of vehicle expenses also generates HST recoverable on most operating costs if you are registered.

- Mixing personal vehicle expenses on the corporate credit card. If you are incorporated, the cleaner approach is to claim a per-kilometre allowance from the corporation rather than putting fuel on the company card.

- Forgetting to update the odometer reading at year-end. Without a Dec 31 reading, you cannot calculate the business-use percentage. Take a photo every January 1.

Why BBA Tax Is the Right Choice for Your Vehicle Deduction Planning

BBA Tax is an Ottawa-based accounting firm that has helped small business owners across Eastern Ontario claim the right vehicle deductions for over a decade. We file T1s for self-employed drivers, T2125s for sole proprietors, and T2 corporate returns for owner-managed Ottawa companies — and the vehicle deduction comes up on most of them.

What makes our approach different: we ask the right questions before you buy or lease, so the deduction is maximized from day one rather than retro-fitted at year-end. We also rebuild prior-year deductions when clients come to us mid-stream, often recovering thousands in missed CCA and operating expenses through CRA T1-Adjustments. If you need help, you can also explore our accounting and tax services for sole proprietors or our dedicated contractor tax services.

We work primarily with Ottawa, Kanata, Orleans, Nepean and Gatineau-area businesses, but we file across Canada via secure portal. Same-day responses during tax season are standard.

Ready to make sure your 2026 vehicle deductions are airtight? Call BBA Tax at (613) 555-1234 or request your free consultation online. We will review your log, your purchase or lease, and your prior-year returns to make sure nothing is left on the table.

Conclusion

The vehicle tax deduction in Canada rewards diligent record-keeping. Keep a kilometre log, save every fuel and maintenance receipt, photograph your odometer on January 1 and December 31, and respect the CRA’s distinction between personal commuting and business travel. Apply the 2026 capital cost ceilings, the $1,100 monthly lease cap, and the $350 interest cap correctly — and you will claim every dollar you are entitled to without inviting a reassessment.

Frequently Asked Questions

What vehicle expenses can I deduct in Canada?

You can deduct the business-use portion of fuel, maintenance, repairs, insurance, registration, lease payments (up to $1,100 per month before tax in 2026), loan interest (up to $350 per month), parking, and capital cost allowance on the vehicle itself. Personal-use portions and fines are never deductible.

How do I calculate the business-use percentage for my vehicle?

Divide your business kilometres by your total kilometres driven in the year. Both figures must come from a written log book. The resulting percentage is applied to all eligible vehicle expenses and to the year’s CCA.

Can I deduct my drive to the office as business kilometres?

No. The CRA treats travel between your home and a regular place of work as personal use, even if you are self-employed or an incorporated owner-operator. Only travel between work sites, to clients, or to suppliers qualifies as business.

What is the CCA limit for a passenger vehicle in 2026?

The 2026 capital cost ceiling is $38,000 before GST/HST/PST for a standard passenger vehicle (Class 10.1) and $61,000 before tax for a zero-emission passenger vehicle (Class 54). Amounts above these ceilings cannot be depreciated.

Should I lease or buy my business vehicle?

Leasing usually produces a larger annual deduction for expensive vehicles kept under four years, because the $1,100 monthly cap allows up to $13,200 of deductions per year. Buying tends to win when you keep the vehicle 5+ years, because once CCA has run its course, the operating expenses still flow through and you own an asset.

Does the CRA accept smartphone mileage apps as a log book?

Yes. CRA accepts digital logs from apps such as MileIQ, TripLog and QuickBooks Mileage as long as they capture date, destination, business purpose, kilometres driven, and the year-start and year-end odometer readings. Export and back up the log monthly.